HANSE Interim | Team RESEARCH: A rolling stone gathers no moss – iron foundries must master challenges

The foundry sector, which is dominated by medium-sized companies, plays an important role in the German economic fabric. Not so much because it makes a major contribution to Germany’s production output (around one percent of the manufacturing sector), but rather because of its value-adding function. For example, hardly any capital goods manufacturer can do without cast components, including bearing housings for wind turbines, engine blocks and cylinder heads for automobiles, plain bearings for rail vehicle construction, machine components, ship propellers, fittings, cast steel nodes for bridge construction and many more.

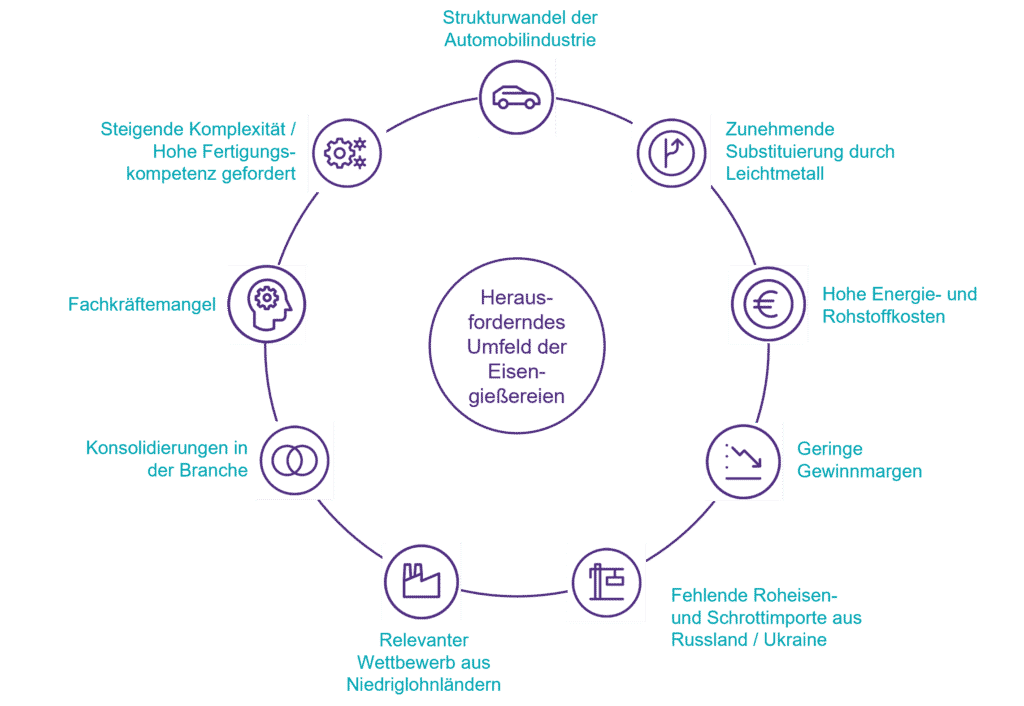

Within the industry, iron foundries in particular have been under pressure in recent years. Suppliers reported shifts in demand toward light metal construction, increasing demands on manufacturing expertise (complexity) and intense competition from producers in low-wage countries, which have become increasingly competitive in terms of quality.

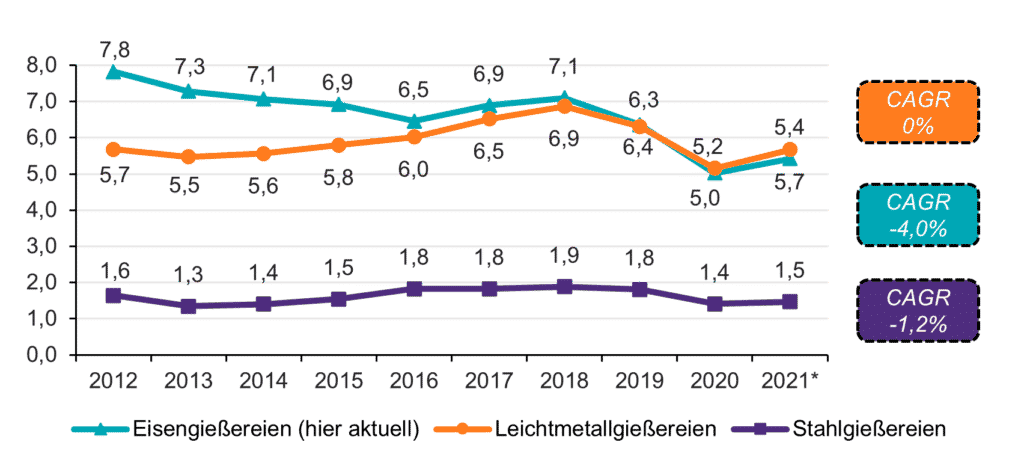

Development of sector sales in EUR billion

Looking at the course of the pandemic year 2020 after a weak economy in 2019, demand from foundries additionally slumped in view of implemented production cuts in important downstream sectors such as the automotive industry.

For many iron foundries, including important suppliers of engine blocks, chassis and brake parts, this represented an additional damper. Against the background of the accelerated shift to electromobility, for example, fewer and fewer iron castings are needed for internal combustion engines or there is a substitution to light metals.

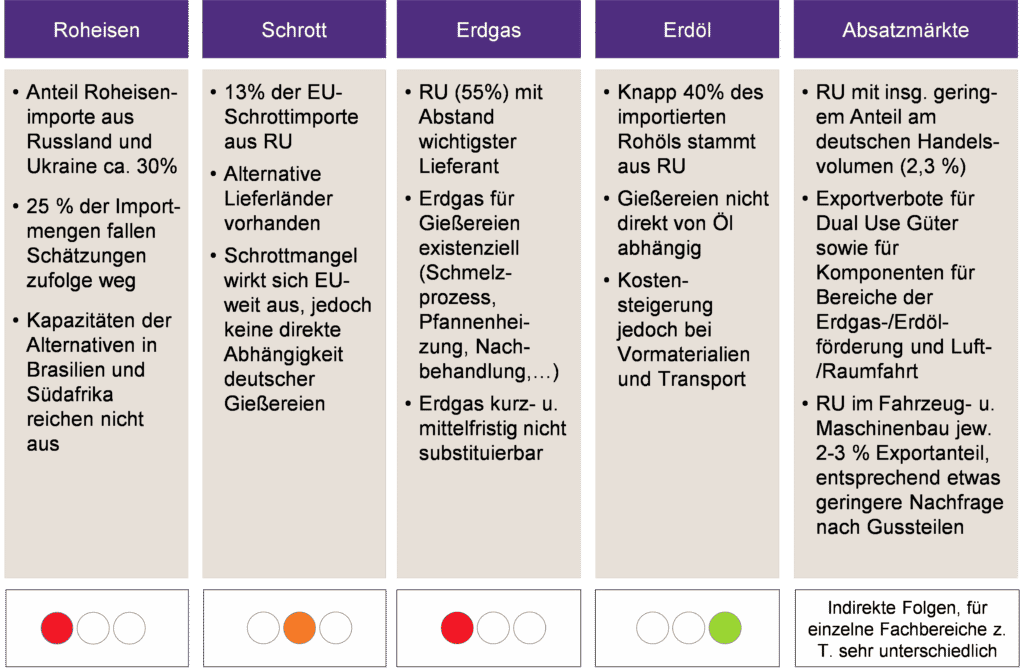

As if that were not enough, in 2020 and 2021 there were also supply bottlenecks and very sharp increases in raw material and energy costs, a situation which was further exacerbated by the start of the Russian war of aggression on Ukraine in February 2022.

Gas prices rose faster than expected, with high uncertainties about the future course. It also dramatically affects the starting materials pig iron and steel scrap which are relevant for the iron foundries.

According to estimates by the industry association, the procurement bottleneck will not be short-lived. Around 25% of the pig iron used in German foundries comes from Russia, which would now be completely lost.

Ukraine crisis and sanctions: Impact on iron foundries on raw materials, energy and sales markets

Tip: Read the article from our HANSE Consulting colleagues titled “Energy costs – Elastic view of hard reality”.

For iron foundries, the challenges are high. Increased costs often cannot be fully passed on in the energy-intensive industry and increasingly it is necessary to expand manufacturing competence, reduce costs, create added value for customers and find customers operating in less shrinking segments or niche markets.

However, innovations are still possible in the iron foundry industry, so that “room for improvement” is always conceivable.

How do you see this change? What challenges do you see for your company?

In our opinion, interim managers and interim experts are currently a well-used instrument in this change environment, for support in innovation and transformation management or also in strategy development. We help you to master your challenges so that you can stand up to your competition.

For a secure and sustainable existence of your company.

We look forward to your contributions to the discussion!

Your HANSE Interim Team

Andreas Lau and Christian Heuermann

Management

Sources: HMC Research Department, IBISWorld, BDG, trade press