Stationary battery storage in Germany: market dynamics, challenges, and opportunities in geopolitically volatile times

Current Market Situation

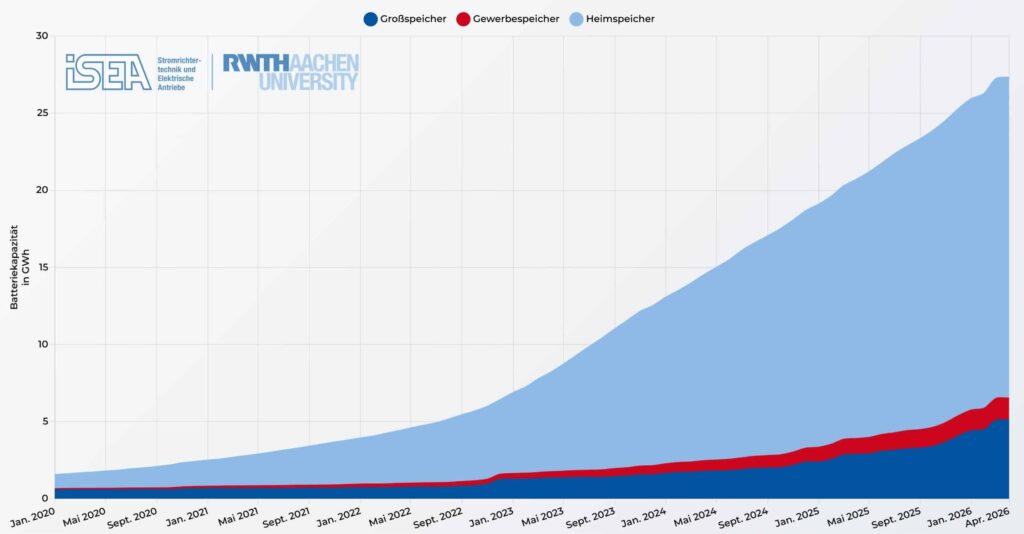

As part of a project for a client in the energy sector, HANSE Interim analyzed key market developments and assessed their implications for future opportunities and risks within the industry. The market for stationary battery storage in Germany is experiencing strong and structurally driven growth. Installed capacity has increased from around 8.5 GWh in mid-2023 to more than 18 GWh by early 2025. By the end of 2025, total capacity is expected to reach approximately 25 GWh. At the same time, the number of registered storage systems has surpassed two million.

This growth is still largely driven by residential storage systems, which account for roughly 80 percent of installed capacity. At the same time, the focus is shifting: large-scale storage is emerging as the most strategically important growth segment.

The underlying driver is clear. The discussion is no longer primarily about the economic optimization of individual applications, but about the stability of the overall energy system.

Integrating renewable energy, managing price volatility, and ensuring security of supply have become central concerns. At the same time, a clear shift within the market segments is becoming visible.

The development of installed storage capacity illustrates both the pace of growth and the changing structure of the market.

In particular, the increasing momentum of large-scale storage systems stands out. What used to be a niche segment is becoming a central building block of the energy system.

Source: RWTH Aachen (ISEA), battery-charts.de, 2026

Structural Challenges

Volatility, Grids, and System Constraints

The rapid expansion of solar and wind energy is increasing the gap between power generation and consumption. Negative electricity prices, redispatch measures, and local grid congestion are becoming more frequent.

Battery storage is widely seen as one of the few short-term levers to address these issues. At the same time, storage projects themselves face constraints: limited grid connection capacity, lengthy permitting processes, and an evolving regulatory framework.

Geopolitical Dependencies

The energy crisis triggered by the war in Ukraine has highlighted the vulnerability of the European energy system. Energy prices are not only higher but also significantly more volatile.

Additional uncertainty arises from geopolitical tensions in the Middle East. Developments involving Iran or the Strait of Hormuz directly affect global oil and LNG markets. Since fossil-based power plants often set marginal electricity prices, these dynamics also impact domestic energy costs.

Supply Chains and Industrial Policy

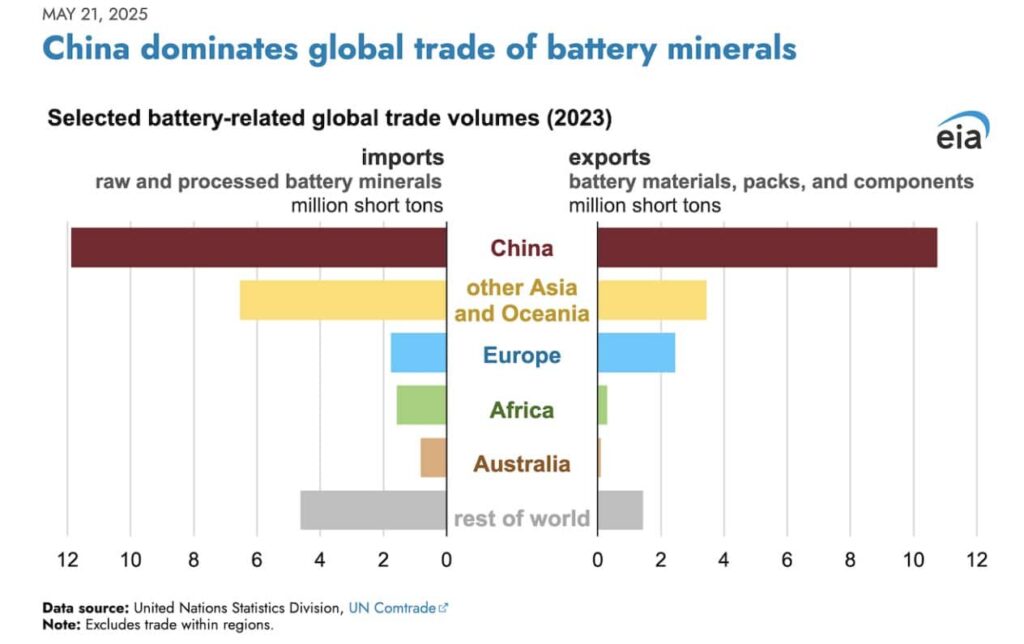

A critical bottleneck lies in the battery value chain. Europe remains highly dependent on imports, particularly from China.

A look at global trade in battery materials and components highlights the extent of these dependencies:

The chart clearly shows that China dominates both processing and exports, while Europe plays a comparatively smaller role.

This dependency is not temporary, but structural – and it has intensified rather than diminished in recent years.

Trade conflicts, export controls, and industrial policy priorities further increase the risk.

Source: U.S. Energy Information Administration (EIA), based on UN Comtrade data (2023)

As a result, battery storage projects are no longer just an energy issue, but also a matter of industrial and geopolitical strategy.

At the same time, current policy debates illustrate the complexity of the topic. As highlighted in a recent analysis, battery storage cannot replace gas-fired power plants in the short term, but it can significantly contribute to reducing system costs and increasing flexibility. The key is not choosing one technology over another, but ensuring an effective combination of both.

Market Trends

From Cost Optimization to Resilience Infrastructure

Battery storage is being redefined. Instead of focusing solely on optimizing self-consumption, the emphasis is shifting toward resilience, stability, and security of supply.

In industry and commerce, capabilities such as backup power, grid support, and price hedging are becoming increasingly important.

The Rise of Large-Scale Storage

Large-scale storage systems are evolving from niche applications into a core component of the energy system.

New use cases include:

- Co-location with large solar and wind farms

- Participation in electricity trading markets

- Grid stabilization services

- Integration into industrial energy management systems

Deployment in this segment has accelerated significantly in recent years.

Technological Diversification

While lithium-ion systems remain dominant, alternative technologies are gaining importance. These include LFP (lithium iron phosphate) batteries and, in the future, sodium-ion technologies.

At the same time, recycling and second-life concepts are becoming increasingly relevant, contributing to a more resilient and less import-dependent storage ecosystem.

Opportunities for Companies and Decision-Makers

Economic Risk Management

Battery storage is becoming a key tool for managing costs and risks.

Typical applications include:

- Peak shaving

- Optimization of self-consumption

- Energy price arbitrage

- Protection against price spikes

This improves planning reliability and competitiveness, particularly in energy-intensive industries.

Strategic Advantage

Energy is increasingly becoming a location factor. Companies that invest early in storage solutions strengthen their operational resilience and reduce dependency on external shocks.

In an uncertain environment, this can be a decisive advantage.

New Business Models

New opportunities are emerging along the entire value chain – from project development and operation to financing and system integration.

Battery storage is evolving from a niche technology into a standalone infrastructure sector with significant investment potential.

Conclusion and Outlook

Stationary battery storage has become far more than just a building block of the energy transition.

It is now a key technology at the intersection of energy, economics, and geopolitics.

Current crises act as accelerators. They expose weaknesses, increase pressure, and at the same time highlight the value of flexibility and autonomy.

For decision-makers, this means one thing: battery storage is no longer a future topic.

It is about competitiveness. And about how resilient business models are in an increasingly volatile environment.

Best regards

Andreas Lau and Özlem Parakenings

for HANSE Interim